A Brewing Bubble In Inflation

A Brewing Bubble In Inflation

Chapter 8, Part II

A supply chain in bondage

Additionally complicating the wage-driven CPI pressures, was a supply chain that was snarled beyond anything seen before, at least in peacetime. Rather than getting better, as it was supposed to, by the fall of 2021, it further seized up. Shipping behemoth UPS announced as the third quarter drew to a close that the logistics industry expected 2022 to be as challenged as 2021. As one wag noted around this time: “How can inflation be transitory if supply chain disruptions are here to stay?”

Further putting lasting upward pressure on prices was the passage of the contentious Infrastructure Bill that finally was signed into law in November 2021. Undoubtedly, America needs a big-time refresh of its roads, bridges, and airports, but the timing of this legislation is problematic. With almost all resources in tight supply and the acute shortage of workers, this legislation is highly likely to shovel more fuel into the inflation blast furnace.

On top of that, there was the even more controversial spending package — the now notorious Build Back Better (BBB) – which was first proposed by Bernie Sanders with an initial $6 trillion price tag. Moderates in Congress whittled that down to a still jaw-dropping $3 trillion. Fortunately, at least for the struggle against even higher inflation, the BBB push stalled at the end of 2021. However, the effort to pass it will likely resume in 2022. Accordingly, the jury is still out as I write this chapter as to whether this will be yet another inflation impetus.

There is little doubt that the various spending packages amounted to a massive overstimulation of the economy, generating a tsunami of additional demand in an already shortage-chocked economy. One could wryly, but rightly, observe that the only thing that there wasn’t a shortage of was shortages. It’s my prediction that the impact of this will persist not only into 2022 but for years to come.

Essentially what we did by practicing de facto MMT was to replace the normal tax-and-spend cycle that Democrats typically resorted to when they were in power — and the GOP wasn’t much, if any, more restrained – with a new model of spend-and-print. Once again, this started under Donald Trump, but Covid gave the perfect cover for it to be taken to an almost incomprehensible level.

As Ben Franklin warned 250 years ago, “When the people begin to think they can vote themselves money, it will herald the end of the Republic.” Mr. Franklin didn’t know about MMT, at least by name, back then. However, he was fully aware of what happened in France a few decades earlier thanks to the French monarchy’s dalliance with John Law’s version, as described in Chapter 6.

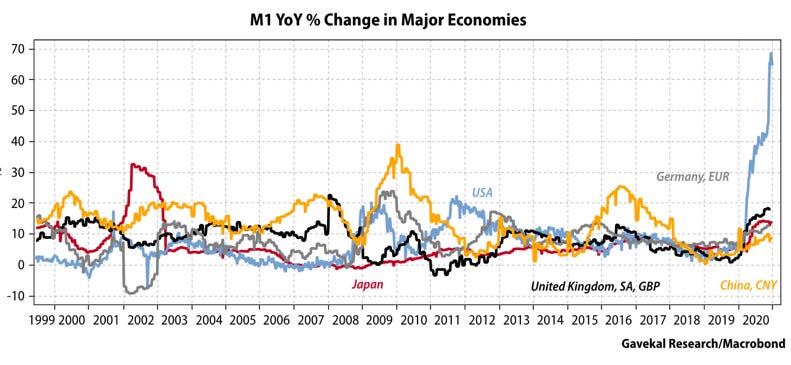

This unprecedented overstimulation of the economy revealed itself in the U.S. money supply as it inflated by 33% in less than 18 months, the greatest surge in 150 years, going all the way back to the Civil War era. Even when compared to Japan’s desperate attempt to print its way out of deflation in the early part of this century, what the U.S. money supply did was simply stunning. Further, there was no effort to remove that money from the system, meaning it will linger there for years to come, with all its inflationary potential.

Figure 7

(M1 = Basic Money Supply)

As we’ve seen earlier in this book, negative real rates, such as prevailed through 2021 and are almost certain to persist in 2022, are also inherently inflationary. As Charles Gave has often pointed out, a prime reason they stoke inflation is that they encourage the leveraged purchase of existing assets (like stocks or cryptos bought on margin and, of course, debt-financed real estate). These asset price inflations frequently came at the expense of making long-term, productivity-enhancing investments such as new plants. Perhaps that’s why capital spending has been deficient for many years per Chapter 7.

Are you getting the sense yet that the Fed’s transitory story might just have a few holes in it? Well, there’s more — even before we get to the hurricane-force inflation-driver in Chapter 9. Louis Gave has pointed out that China’s One Child policy is coming home to roost. As previously discussed, China and its rock-bottom labor costs, were a significant and structural deflationary factor for at least 20 years. This was in no small part due to the fact that its labor force was growing by 10 to 15 million workers every year.

Now, though, thanks to its looming population shrinkage due to One Child, it is set to contract by 5 to 10 million annually. As Louis notes, this is a classic example of a government intervention that has gone awry, at least if you want to believe the transitory inflation narrative. With big government on the rise pretty much everywhere in the world these days, that’s yet another inflationary force. (To access excerpts from Louis Gave’s essay on how China’s demographic challenges will influence global labor costs, please see the Appendix.)

From delight to fright

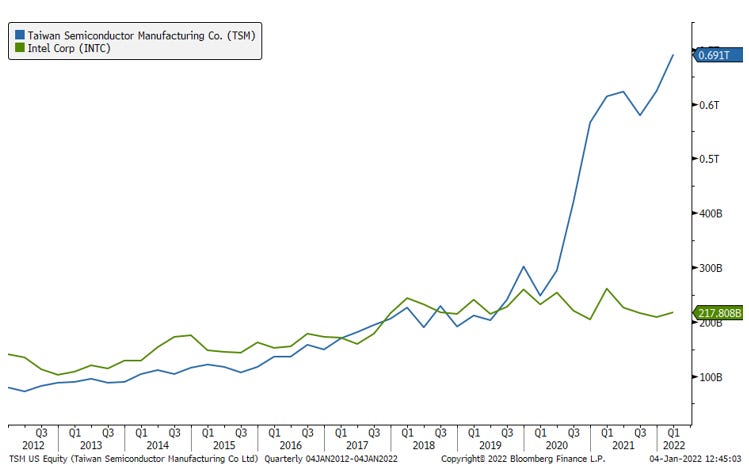

It’s a similar story with the all-important semiconductor supply situation. The China trade war that started under Donald Trump, which denied Chinese tech companies access to critical American components such as semis, caused its government to launch a frantic effort to build its own semiconductor industry. One reason being floated for why China might invade Taiwan is to secure control over the most valuable and cutting-edge integrated circuit company in the world, Taiwan Semiconductor. As you can see, Taiwan Semi’s market value now greatly exceeds Intel’s, reflecting the former’s increasing dominance.

Figure 8

In turn, the U.S. is pressuring companies like Intel and Taiwan Semi to build new plants in the U.S. to ensure access to this basic building block of nearly all things tech related. Accordingly, supply chains are being shortened, by bringing production closer to end markets. However, this has the effect of making products, including semis, more expensive. Illustrating this was Taiwan Semi’s 2021 price hike, so unusual in the tech world where, historically, prices have typically consistently gone down.

A wide range of Asian tech players are raising prices, a previously unheard-of development. Moreover, there is an acute shortage of semiconductor substrate in the autumn of 2021. Our excellent tech analyst, Arnaud Legland, sees an extremely tight market for another critical semi component, wafers, starting in 2022 with little hope of new supply coming on-line anytime soon. (Arnaud does see a number of semi products becoming oversupplied as 2022 matures.)

As Pimco’s former CEO Mohamed El-Erian wrote in the Financial Times in September 2021, “The dominant structural theme post the financial crisis — that of deficient aggregate demand — has given way to frustrating supply rigidities. They are not going away soon.” (Emphasis mine) If he’s proven right over time, as I clearly think he will be, this is highly likely to be a concussing shock to most investors who, as I’ve conveyed, remain convinced the Fed has the inflation situation under control. This is true even as Jay Powell reluctantly conceded in December 2021 that the term “transitory” needed to be “retired”. However, it’s those kinds of unpleasant epiphanies — when the majority of investors realize they’ve been betting on the wrong horse, like inflation coming down to around 2% by the end of 2022 — that create market convulsions.

This pervasive faith in the Fed has long puzzled me. As The Wall Street Journal pointed out in a July 29th, 2021, opinion piece: “The Federal Reserve employs hundreds of economists whose job is assessing the American economy. So it is remarkable that the Fed is so wrong so often in its economic forecasts. The latest big miss has been its failure to anticipate this year’s surge in consumer prices.”

Unlike the Fed, I did believe inflation was coming our way soon. Here’s what I wrote in the Evergreen Virtual Advisor (EVA) newsletter as far back as late October of 2020, when inflation was still MIA: “With Modern Monetary Theory (MMT) giving US politicians from both parties the green light to spend like they never have before, at least in peacetime, financed by the Fed’s MMM[iii], it’s just a matter of time, in my opinion, before we have both a weaker dollar and higher inflation. Policymakers might be delighted at first with inflation moving above 2% but when and if (I think it’s when, not if) it hits 4% or even 5%, that delight is going to turn into fright very quickly.”

It was a good, but not perfect, call: While inflation did move into the 4% to 5% range — actually, nearly 6% based on the social security hike – the U.S. dollar performed remarkably well in 2021. This is almost certainly due to the fact that most major Western countries pursued similarly incontinent fiscal and monetary policies. However, China and Russia — our, once, present, and future geopolitical rivals — have not been; thus, it’s interesting that the Renminbi rose slightly vs the USD in 2021 while the Ruble was essentially flat. Against most other currencies, the dollar rose throughout 2021.

Figure 9

Also, while it’s true a number of influential individuals began to publicly express concerns about inflation, the Fed was able to convince most politicians, and certainly the markets, that it’s a fleeting phenomenon, despite the trash-canning of “transitory”. However, former Treasury Secretary Larry Summers was not one of them. In the summer of 2021, he warned, “The Fed has had almost no success in bringing down prices once the economy has overheated.”

Regardless, the Fed has repeatedly and vehemently told the world it has all the tools it needs to bring inflation back down should it prove sticky. To which I say, “No way, Jay!” It has been my view that the Fed lacks the fortitude to take the type of extreme tightening needed to rein in truly virulent and persistent inflation. In fact, I believe Jay Powell has become the anti-Volcker.

Moreover, at this juncture, I have begun to suspect the Fed wants much more inflation than it has admitted — as long as it convinces the rest of the world of the opposite. The aforementioned Luke Gromen wrote extensively on this even before Covid hit. His basic view, in short form, is that the only way the U.S. government can cope with its nearly $30 trillion of official debt, and the off-balance sheet $100+ trillion (note the plus sign) of entitlements, is to do what America did after WWII.

Essentially, the U.S. kept interest rates low (as was the case in 2021, the Fed bought bonds to keep rates suppressed) while the economy boomed and inflation soared. The CPI rose by 20% at times in the late 1940s but interest rates were held in the 2% to 3% range. The economy grew by an average of 7.2% from 1946 to 1952 on a nominal (i.e., including inflation) basis. As a result, the debt-to-GDP ratio fell from about 115% to roughly 70%. In other words, the strategy worked, and a debt crisis was avoided. Of course, bond investors were the sacrificial lambs, as inflation destroyed the purchasing power of their holdings.

Per Luke Gromen: “When the US government borrows from its own domestic investors at negative real rates, the US government is actually stealing real wealth from its own citizens (effectively a sort of tax increase on a real basis).” He also wryly, but rightly, observes that: “Importantly, a key part of inflating away one’s debts is convincing one’s creditors that one is not inflating away one’s debts.”

To that last sentence I would add: like convincing them that the current high inflation rate is abnormal, even if no longer transitory. In Chapter 9, I’ll finally address the intense inflationary force that I believe ranks right up there with MMT in undercutting the Fed’s “we’ve got this” storyline.

[iii] Its Magical Money Machine, as described earlier.