A Brewing Bubble In Inflation?

A Brewing Bubble In Inflation?

Chapter 8, Part I

Maybe “transitory” was the real transitory

Throughout 2021, there was likely no more pressing question for investors, and consumers, than this: “Was inflation truly transitory?” As described earlier, that’s certainly what the Fed wanted the world to believe.

It’s my view that high and rising inflation is the most likely factor that would terminate the Fed’s go-to reaction for nearly all threats: hitting Control + Alt + Print. This is because printing more trillions from its Magical Money Machine would only escalate inflation anxiety if it was thought to have become entrenched. Without the Fed downside protection mechanism (that now legendary Fed Put), both stocks and bonds would have to sink or swim based on actual fundamentals and free-market demand. For financial markets, this would be a most disruptive development. As you may have observed, these interrelated events are beginning to play out in early 2022.

So far in this book, I’ve just touched on inflation other than arguing that conditions are much different than in the past 40 years and, of course, in Chapter 6, that history is clear that Modern Monetary Theory-type policies are inherently inflationary. Now, though, let’s consider in detail the manifesting array of more conventional inflation forces. Far from trivial, you will see they are, in fact, paradigm shifting.

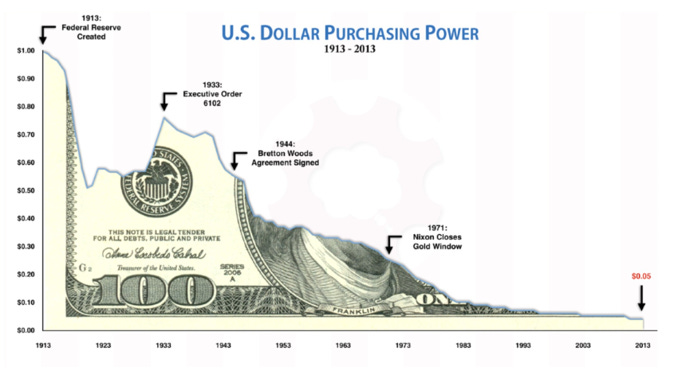

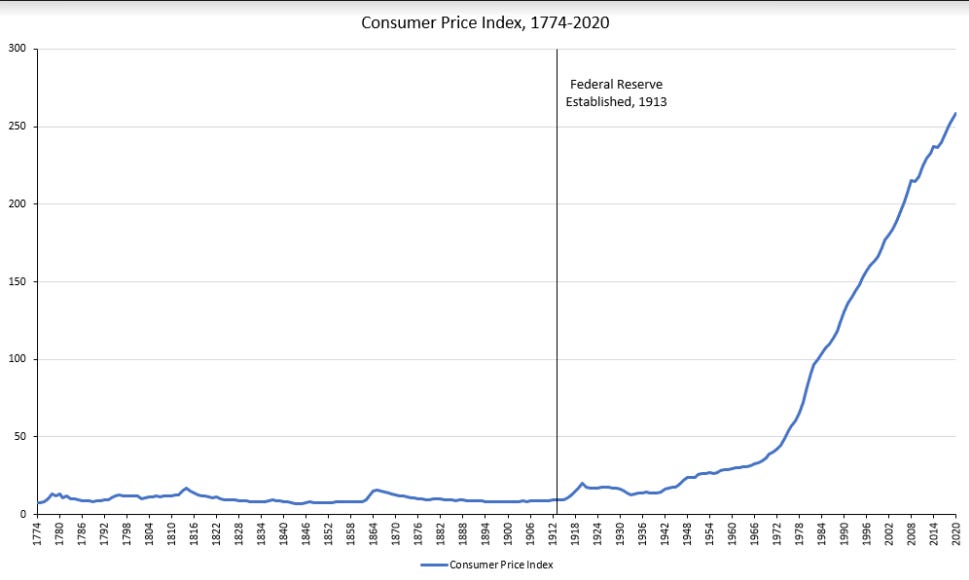

It’s sobering to consider the two images below, especially in the context of four decades of relatively benign inflation. Clearly, something big happened in the early 1970s and, as noted previously, that was Richard Nixon pulling America off the gold standard.

Figure 1

Figure 2

Equally obviously, a game-changer also occurred right before WWI. If you’re not sure what that was, please allow me to remind you this was when the Federal Reserve was established. As you can see, basically from the founding of the Republic until the establishment of the Fed, the U.S. dollar held its own in purchasing power, except during the Civil War. Even that erosion was reversed in fairly short order due to a number of years of deflation. It’s important to point out that America enjoyed unprecedented growth in its economy during its first 130 years of existence, prior to the Fed’s creation, despite many boom-and-bust cycles.

Of course, since 1971 and the departure from the gold standard, the greenback’s decay has become even more pronounced. Yet, most Americans have felt comfortable with the Fed’s target of 2% per year purchasing power erosion despite that it means a 45% haircut over a 30-year period

Maybe that sanguine attitude was due to the fact that, as we’ve seen in earlier chapters, for most of the past 40 years it was possible to earn more than inflation with bonds and, often, federally insured certificates of deposit. But, as we all painfully know now, those days are long gone.

Frankly, that’s a big part of the inflation resurgence thesis of which I have become an ardent proponent. Millions of investors and savers are waking up to the reality that holding U.S. dollars, even including earned interest (such as it is), is a losing proposition. Thus, it’s much better to play the stock market or buy hard assets, like real estate, or not-so-hard assets, like cryptos, rather than stay in cash. When expectations become widespread that cash is trash, inflation can quickly become a societal problem.

By the fall of 2021, this had become a major consideration due to the fact that U.S. households were sitting on around $2.5 trillion of excess savings[i] and inflation was worsening, despite the Fed’s constant protests to the contrary. This massive savings cache had been accumulated since Covid blessed us with its presence and was a direct function of the federal government’s trillions of support payments. With Delta and then Omicron keeping things subdued in the second half of 2021, that money didn’t move much, other than into stocks, cryptos and other risky assets. However, given American consumers’ propensity to do what they do best — consume — I suspect this immense stash of cash won’t remain dormant. This is likely to be especially the case if Mr. and Mrs. America believe they better buy now because almost everything will cost more next year or, even, next month.

When Fed chair Jay Powell was getting grilled in Congress in July 2021 — as it was becoming obvious inflation was running much hotter than the Fed had anticipated – Senator Cynthia Lummins pointed out to him that U.S. households “… are sitting on deposits and close substitutes of equivalent to 79% of GDP” up from an average of 51%. “Is it really wise,” she went on to ask him, “to continue to have accommodative policy where there’s still trillions of household cash that will flow into the economy soon?” Mr. Powell looked at his watch as she was speaking and obfuscated as he has done so often in recent years – not to mention repeatedly contradicting himself, even in the same speech or reply. (Source: Grant’s Interest Rate Observer)

As far back as the summer of 2020, Wharton Professor Jeremy Siegel, well-known for his typically rosy view of the economy and the stock market, was picking up on the mounting inflation threat. Per Prof. Siegel, “The money created by the Fed is not going only into excess reserves of the banking system (as it did in the earlier QE rounds). It is going directly into the bank accounts of individuals and firms through the US Payroll Protection Plan, stimulus checks and grants to state and local governments”. He presciently predicted “… an extremely inflationary economy in 2021”, as early as mid-2020, per the above, when almost no one, including — make that, especially – the Fed, saw it that way.

The official inflation numbers during the second half of 2021 were certainly husky but it’s perhaps a stretch to call them “extremely inflationary”. However, Jeff Gundlach opined in his September 2021 webcast that if housing price increases were included, the CPI would be ripping at 12%, a number that certainly qualifies as extremely inflationary. This relates to my earlier examination of how the Fed’s OER (Owners’ Equivalent Rent) has understated the stunning increase in home prices this century/millennium.

Mr. Gundlach, the reigning King of Bonds, also believes the triple whammy of trillions of Federal red ink, financed by trillions of the Fed’s fantasy funds, and a hemorrhaging trade deficit, are going to be Kryptonite to the mighty U.S. dollar. Again, looking back over the last 40 years, the dollar has been strong against most major currencies. That has definitely helped keep inflation at bay.

The odds stack up against transitory

Should the buck fall hard, as Mr. Gundlach believes (in the summer of 2021 he referred to it as doomed, long-term), this will be another source of upward pressure on the CPI, as well as the PPI, the Producer Price Index. This is a function of the reality that a weaker dollar pushes up the price of imported goods.

Then there is the Fed itself and its changed and expanded mandates. It has been LCD clear that it will let the economy run hot to bring down unemployment. As a reminder, since 1978 its mission statement has been to keep inflation in-check and the jobless rate subdued. Now, the latter appears to be Job One and the former… well… not so much. This is despite the fact that, toward the end of 2021, Jay Powell began to pay lip service to controlling inflation — even as he maintained the easiest monetary policies in U.S. history, save for a few months earlier.

In my view, Powell & Co. would be well-advised to deeply reflect on this quote from former senior Fed official, William Poole: “The idea that we can let down our guard on inflation to increase employment is unwise in the long term because higher inflation eventually destroys rather than creates jobs.” (Emphasis mine) It’s a lesson that central bankers — and the planet — learned the hard way in the 1970s but, apparently, it has been unlearned in recent years.

Moreover, as I’ve also described in earlier chapters, the Fed is now under extreme political pressure to fight climate change and address racial economic inequities. On September 15th, 2021, a bill was introduced in Congress that would force the Fed to punish banks for lending to fossil fuel producers. (More on this in Chapter 9).

As far as narrowing the wage differential between whites and minorities, the Fed has made it clear it sees keeping the unemployment rate down as critical to this, even if it means more inflation. Perhaps that is admirable from a social justice standpoint, but it’s for sure another upward force on consumer prices. Moreover, there is the critical issue that the poor suffer the most from inflation surges. In his January 6, 2022, “The Flow Show” BofA’s Michael Harnett noted that “the price of basic human needs such as food, heat, shelter (are) soaring; global food prices rose 27% year-over-year; US heating costs up 30% for natural gas, 43% for oil, 54% for propane; US rents up 12%, house prices up 18%.” Attempts to mitigate these hardships with wage and price controls, which might be poised to make a comeback in modern day America, are notoriously counterproductive. (Please see the Appendix for additional thoughts on this topic.)

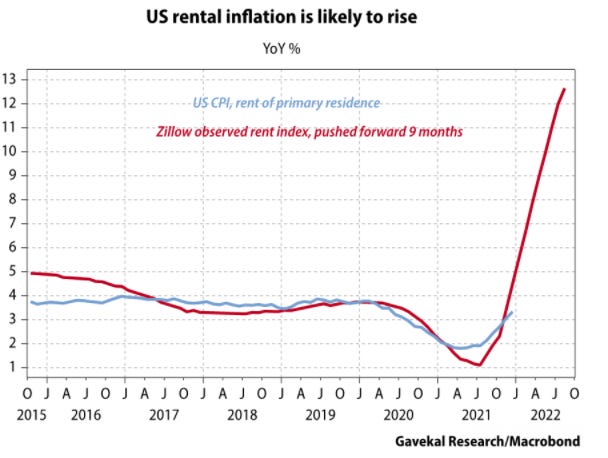

Quoting my digital mate and fellow financial newsletter scribe, Sydney-based Gerard Minack: “The fact that the Fed has promised not to be pre-emptive in this cycle is the single most important reason to expect a second wave of inflation.” By “second wave”, he’s making the crucial point that during the first part of 2021, the CPI surge was due to commodities, like lumber, going vertical along with new and used cars. He correctly foresaw those pressures easing. This backing off caused many in the investment community to take it as validation of the Fed’s transitory thesis, at least for a while.

Yet, like me, Gerard sees this as a head-fake, hence the second wave part of his argument. He anticipates rent inflation to become a far more persistent inflationary impulse along the lines of a looming spike by the aforementioned OER.

Figure 3

Moreover, also simpatico with this author, Gerard thinks labor costs are heading in a decidedly northerly direction. As he wrote in his July 20th, 2020, Down Under Daily, (definitely not a “DUD” of a read, by the way): “For now, signs of a tight labor market are everywhere but in the wage statistics.”

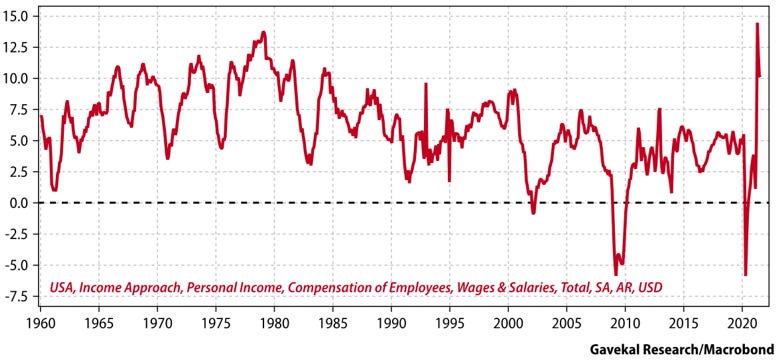

Perhaps that’s because of the archaic way they are measured. Another financial newsletter compatriot is Ben Hunt of Epsilon Theory. He contends that the U.S. generated more wage inflation over the four quarters from March of 2020 to March of 2021 than at any time in the prior four decades. Ben believes the Bureau of Labor Statistics is understating wage inflation by using a century-old approach of tabulating hourly wages versus today’s far more prevalent salary-based compensation. The following Gavekal chart certainly indicates that Ben, and Gerard, are on the right scent.

Figure 4

François Trahan, voted the number one portfolio strategist on Wall Street for 8 of the 10 years from 2009 to 2018, pointed out in a September 2021 research missive that the supply of labor leads wage inflation by about a year. Wage inflation, in turn, leads core inflation by another year. Based on the extremely tight job market as the year progressed, with small business openings at a two-decade high (by far), there would appear to be considerable wage inflation in the pipeline, as the below chart clearly indicates. This will make a significant CPI cool-down even less likely in 2022.

Figure 5

(Source: Goldman Sachs, 11/18/21)

My close friend Vincent Deluard, Director of Global Macro at International Stone X, believes the Fed is overlooking a critical change in the overall employment situation. In cliff note form, he is convinced it is missing the millions who are now employed in the “gig” economy, such as folks working for Uber. These individuals typically don’t have income tax withheld and, in many cases, might not report their income at all if it is paid in cash.

Yet, millions must be reporting their earnings because, per Vincent, in the first half of 2021, the Treasury collected $308 billion in non-withheld personal income taxes, up 110% from 2019! Another shocker is that this number was materially larger than the $230 billion the U.S. treasury brought in from corporate taxes in the first half of 2021. As he concedes, not all non-withheld personal income tax is from gig workers but the fact that this number exploded as the gig economy took off certainly indicates it’s been a big factor.

Vincent further observes, “Yet, the statistics the Fed uses to model the economy ignore this massive and soaring portion of the economy… The Fed’s lack of data on the… gig economy will likely lead it to overestimate the slack in the labor market.” If he’s right, and his logic is persuasive, the Fed has been making a prodigious mistake by continuing to print $120 billion a month throughout almost all of 2021 in its attempt to force down the unemployment rate when the labor market is already speedo-on-a-Sumo-wrestler tight. This has significant inflationary implications.

To put more color on just how robust the U.S. employment picture was in the fall of 2021, job openings were nearly 1 million above new hires, a record spread. Additionally, the Quit Rate, which measures those workers voluntarily leaving their current employers, presumably for higher pay in most cases, has been in a powerful uptrend.

Figure 6

Then, of course, the federal government has been paying generous unemployment benefits, creating a disincentive to return to work. The support payments were essential during the worst of the lockdowns. However, even early in 2021 there were countless businesses — large, small and in-between — desperate for workers, causing this policy to become exceedingly counterproductive. Unquestionably, it is yet another factor contributing to a severe shortage of employable individuals.

There was another force lurking in America’s labor market at the time, one that threatened to make conditions even more nightmarish for businesses, including hospitals, to retain their workforces. It’s a trend that pundits like Luke Gromen began referring to as “The Great Resignation”.

This referenced the swelling wave of American workers refusing to be vaccinated and choosing to retire or, I suspect, in millions of instances, opt to work in the aforementioned gig economy. The latter might not be quite as deleterious as the former because theoretically jobs are still being filled even if they aren’t part of the official economy. By the time you are reading these pages, we’ll know how great — or un-great — this resignation movement became but I would venture to say it will be another blow to keeping wage inflation in check. As I write these words, it’s hard to find a company that isn’t desperate for workers. In reality, they were often so hard-up they were forced to shut down, or, for those with the means, to dramatically raise compensation.

The remarkably lucrative settlement John Deere workers agreed to in late November 2021 is a graphic, and most telling, example of the latter. Its union was able to secure for its members an upfront 10% raise, an $8500 signing bonus, further 5% pay bumps in the third and fifth years of the six-year contract, and 3% hikes in the second, fourth, and sixth years.

Yet, the biggest eye-opener, at least to me, was that this deal reinstituted a cost-of-living adjustment, also known as a “COLA”. These were a hallmark of the inflation-riddled 1970s, but they had largely faded away since the 1980s. The fact that these are making a comeback is extremely ominous from the standpoint of avoiding the dreaded wage-price spiral. Even in Europe, where chronically high unemployment has kept a tight lid on labor costs, COLAs are reappearing.[ii]

Of course, that’s what the Fed wants: higher pay for the rank and file. The problem is that, as many began to notice during the early fourth quarter of 2021, inflation was eating up all or more of the wage gains. Rising compensation only helps workers if it outpaces the CPI which, for all the reasons we’ve seen, has become a steep hill to climb.

Section II To Be Released February 23rd

[i] In other words, U.S. consumer savings has increased by around $2.5 trillion since pandemic began.

[ii] Vincent Deluard is one of the few pundits I know making the important point that COLA adjustments on social security payments are creating a much broader wage-price spiral than is generally understood. Even though these benefits are not technically wages, the inflation impact is the same. With tens of millions of now retired Boomers, and another nine million Americans disabled, thus collecting benefits, this equates to around 40% of America’s labor force. Accordingly, COLAs have quickly become extremely pervasive… and inflationary.