Bye-Bye, Buyback Bubble?

All “good” things come to an end

Returning to the opening of this chapter, what might be the death-knell of buybacks? For sure, the highest corporate debt levels relative to the size of the economy are a possibility. However, it would probably take a spike by interest rates, a recession, and/or a surge in defaults to stop this insider enrichment process. (It’s worth observing that, as I write these words, inflation getting out of control could bring about all three of the above nasties.)

Another more immediate threat might be political. Pols on both sides of the aisle have buybacks in their crosshairs. Unsurprisingly, Bernie Sanders and Elizabeth Warren have railed against them. But when you hear someone like the GOP’s Marco Rubio attacking them, that’s a much more serious threat. (Please refer to the Appendix for Sen. Rubio’s criticisms of the S&P 500 constituents’ addiction to buybacks.)

Similar to his sentiments, since 2000, $6 trillion was expended on buybacks while personal income wages were up a far lower $3.5 trillion. That’s the kind of discrepancy that attracts the ire of Congress which is, as I write this, threatening to tax buybacks.

Done selectively and judiciously, there is certainly nothing inherently wrong with companies retiring their own shares. In fact, when executed at low prices, where the effective equity yield is high, they can be extremely rewarding to shareholders. For example, if a company is selling at 10 times its annual profits, its earnings yield is 10%. ($10 of earnings on a $100 market price.) If it can safely borrow money at 4%, or has cash sitting around yielding next to nothing, buybacks are value-enhancing for shareholders. However, if the P/E is 20, then the earnings yield is only 5% and the benefits become pretty skinny. The latter situation is much more common these days with the S&P trading around twenty times hoped for 2022 earnings.

A tangible example of shareholder value-enhancing buyback activity was what U.S. energy companies started doing with gusto in 2021. As noted in Chapter 9, energy producers began using the cash flow gusher they received as both oil and natural gas soared, particularly in the second half of the year, to repurchase their own shares at very high free cash flow yields. (See Glossary)

Unfortunately, such a shareholder-friendly manifestation of share repurchases has become the exception, not the rule. Frankly, most companies have no business wasting precious shareholder capital by wildly acquiring their own shares with the overall S&P 500 at one of its loftiest levels ever.

To put things in perspective, in 2018 and 2019, S&P 500 companies spent $1.5 trillion on share repurchases, 50% more than they paid out in dividends, an amount equivalent to the value of all the gold that’s ever been mined (but only around half of Apple’s market cap!). As pointed out above, due to Covid, buybacks cratered… briefly. But that pause was enough to bring about a rare down year for repurchases. However, in 2021, buybacks, at least based on authorizations, were on pace to hit an all-time high.

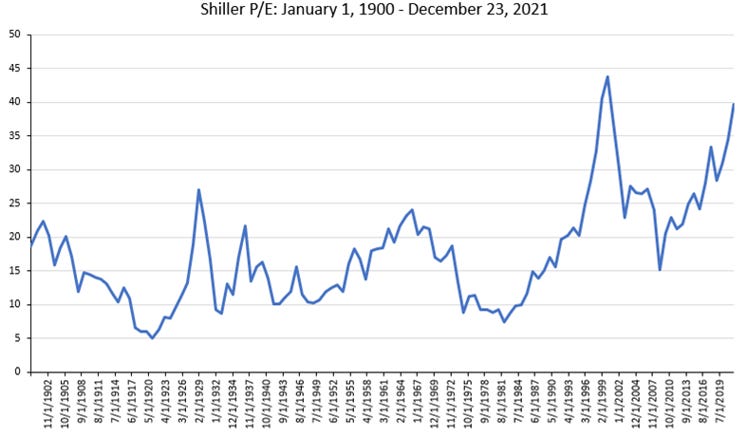

As BofA Merrill Lynch strategist Savita Subramanian has observed: “Buybacks work when there’s scarcity value. Now everyone’s doing it.” To her point, 60% of companies have done repurchases. And they are doing so at a time when, per figure 13 on the price-to-sales ratio, one of the best metrics for predicting long-term returns, is higher than it was in early 2000, at the tech bubble’s apex. This buyback binge is also occurring when the Cyclically Adjusted P/E (CAPE) is pushing 40. The latter is also known as the Shiller P/E ratio, named after Yale’s esteemed Prof. Robert Shiller. While it’s not quite as high as it was in early 2000, compared to all other prior peaks it’s extremely elevated, even above where it was in 1929.

Figure 14

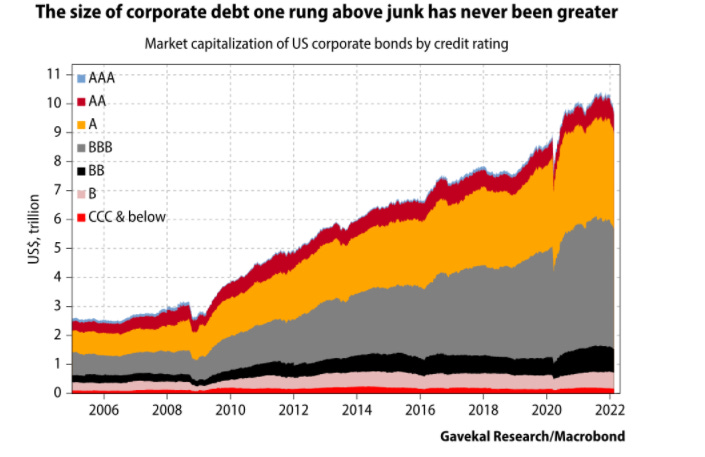

The dark side of this shareholder cash return frenzy was that it pushed net-debt-to-cashflow to a 16-year high on the eve of the pandemic. This was a direct result of dividends and buybacks running above the available cashflow necessary to fund them since 2013.

Similarly, the ratio of Corporate America’s enterprise value (EV) relative to its aggregate cash flow is at an all-time high. (EV means equity and debt values combined.) In other words, both debt and equity valuations relative to cash flows are extremely elevated. As noted at the outset, prudent companies are careful not to let their debt/equity ratios get out of line even when spending on growth initiatives. Sadly, prudence has been increasingly MIA in corporate boardrooms in recent years.

Figure 15

To elevate debt to dangerous levels to enable share repurchases — which usually lowers profits because of the increased interest costs — is the antithesis of judicious corporate stewardship. When this chapter first ran, I opined that this wasn’t likely to become an issue until the next recession. Little did I know then that it was mere weeks away and that it would be one of the most severe, despite its brevity. Notwithstanding that the Covid recession only lasted a month, the nearly overnight shutdown of most of the global economy had a profound impact on buybacks. Basically, repurchases collapsed with profits.

Figure 16

Due to intense rating agency pressure myriad publicly traded U.S. companies were forced to suspend buybacks, per Figure 11. This was a great misfortune for shareholders as many were down 50% or more. This created exactly the opportunity for which capable and prudent management teams hope when it comes to repurchasing their own shares. To make matters far worse, a large number were forced to sell shares, as we will soon see.

Even prior to Covid, there were sneak previews of the coming horror film. As covered in a number of our newsletters as it was devolving, GE was a badly tarnished example of this phenomenon. It bought back tens of billions in stocks at high prices, and then was forced to issue equity at depressed levels to strengthen what became a precarious financial condition. Some accounting experts were even predicting it would become another Enron. (Fortunately for its long agonizing shareholders, it appears to have finally found a CEO, Larry Culp, who has been able to repair at least some of the damage; appropriately, he is the son of a welding shop owner.)

Mining and energy companies did the same thing. They were aggressive buyers of their own shares during the boom years of the early twenty-teens. Then, after each industry’s bust, many were forced to sell shares on the cheap to shore up their weakened balance sheets.

Cruise lines, hotels, theaters, restaurants, department stores and all of the other prime victims of the pandemic had near-death experiences, and many were forced to sell shares to stay afloat (literally, in the case of Carnival and Royal Caribbean). This was despite hundreds of billions of federal bail outs. And, in most cases, these companies had been aggressive buyers of their own shares prior to Covid.

Naturally, politicians were further incensed that a plethora of companies, which had been employing the management enrichment technique of overpriced share buybacks, were now using taxpayer money to stay alive. There was much discussion of bringing back the same requirement that, in return for survival funding, the Treasury would be awarded warrants. As we saw earlier, these made the U.S. government (and, hence, taxpayers) lush—and unexpected--profits after the Great Recession. However, a few firms, like Boeing, refused and, inexplicably, the government acquiesced. As a result, huge gains for taxpayers were forfeited.

Unquestionably, the speed with which the economy and the stock market recovered was why the cacophonous uproar over buybacks died down just as quickly. As we’ve seen before, like with winning in sports, a raging bull market is a powerful deodorant. However, in my opinion, Corporate America is setting itself up for another thrashing as it madly repurchases shares at even more overvalued prices.

Although the Banana Republic monetary policy of MMT has delayed the day of reckoning – when it is revealed how much overpaying has occurred – rest assured that it’s very much a case of postponement, not cancellation. As you may have noticed, the concept of an inevitable payback, due to the countless can-kicking tricks to which our policymakers have repeatedly resorted, is one of the main messages of this book.

Gotta pay for all those ‘management options plans!’ Also helps management qualify for their stock awards in their comp packages!