Green Energy: A Bubble In Unrealistic Expectations

Green Energy: A Bubble In Unrealistic Expectations

Chapter 9, Part I

Europe’s shocking energy crisis

As I wrote previously, it amazes me how little of the debate in 2021 centered on the inflationary implications of the Great Green Energy Transition (GGET). Perhaps that’s because there is a built-in assumption that using more renewables should lower energy costs since the sun and the wind provide “free” power.

However, we will soon see that’s not the case; in fact, it’s my contention that it’s the opposite, and I’ve got some powerful company. BlackRock CEO Larry Fink, a very pro-ESG[i] firm, is one of the few members of Wall Street’s elite who admitted this in the summer of 2021. The story, however, received minimal press coverage and was quickly forgotten (though, obviously, not by me!).

This chapter will outline myriad reasons why I think Mr. Fink was telling it like it is… despite the political heat that could bring down upon him. [ii] First, though, I will avoid any discussion of whether humanity is the leading cause of global warming. For purposes of this analysis, let’s make the high-odds assumption that for now the green energy transition will continue to occur. (For those who would like a well-researched and clearly articulated overview of the climate debate, I highly recommend Unsettled by a former top energy expert and scientist from the Obama administration, Dr. Steve Koonin.)

The reason for the italicized “for now” is that I think it’s extremely probable that voters in many Western countries are going to become highly retaliatory toward energy policies which are already creating extreme hardship. Even though it’s only early autumn as I write these words, energy prices are experiencing unprecedented increases in Europe. Because it’s “over there”, most Americans were only vaguely aware of the severity of the situation. But the facts were shocking…

It was a perfect storm on the Continent as the fall of 2021 turned into the winter of 2022. Or perhaps it was the perfect non-storm as a major culprit in Europe’s current energy crisis has been a general lack of wind, becalming its array of windmills. It’s also been unusually cloudy, which is saying something, especially for Northern Europe, inhibiting solar power output. Further, temperatures have been somewhat colder than normal, though not nearly to the degree — or very low degrees – which China is facing. This has left natural gas storage levels critically low. (Fortunately for the Continent, thus far the actual winter has been relatively mild.)

Consequently, “nat gas” prices went truly postal at the end of last year reaching roughly $170 per MegaWattHour (MWh) in late December, the highest ever. Now get ready for this one: that’s eight times what it was a year earlier. This has driven electricity prices to the equivalent of $250 per barrel in oil terms! Obviously, the term crisis isn’t hyperbole “over there”. In fact, I’d suggest it has truly become a mega-crisis. (As of early February 2022, electricity prices have been cut in half, thanks in part to a 40% surge in U.S. liquified natural gas shipments to Europe; yet they are still four times their year ago level.)

Per best-selling author Bjorn Lomborg, 50 to 80 million Europeans were suffering from severe energy poverty even prior to the estimated $400 billion power cost surge in early 2022. Additionally, six million UK households may not be able to pay their energy bills this winter. In fact, because of this unprecedented energy cost explosion, the British populace is facing the most severe drop in living standards on record. Widespread social upheaval in Europe is a distinct risk considering that gas pump hikes of just 12 cents per gallon in France produced widespread unrest. Lending credence to this concern, the bloody riots in Kazakhstan in early January 2022, which caused Russia to send in paratroopers, were primarily attributed to surging energy costs.

Besides the escalating human suffering, which threatens to be truly catastrophic should the last month of winter 2022 turn out frigid, it’s also producing a boom in coal power. The Continent’s coal plants are running full out and lignite, the dirtiest of coal sources, is dominating the fuel mix. Therefore, Europe’s energy agony is also aggravating environmental degradation. As we should all know, using coal as an electricity feedstock is far more polluting than oil and, especially, natural gas.

Aggravating the growing humanitarian crisis, serious food shortages were developing after the exorbitant natural gas price surges forced most of England’s commercial production of CO2 to shut down. Per the London-based Financial Times during the fall of 2021: “Soaring gas prices have forced the closure of two large UK fertiliser plants, sparking warnings of a looming shortage of ammonium nitrate that could hit food supplies as record energy prices start to reverberate through the global economy.”

Please check out this chart from the super-savvy team at Doomberg that shows the literally vertical move in North American fertilizer prices. Moreover, the US and Canada have a tremendous cost advantage due to far cheaper natural gas which is a critical fertilizer in-put.

Figure 1

Source: Doomberg, Doomberg

Normally, I’d say the cure for such extreme prices, was extreme prices, to slightly paraphrase the old axiom. But these days, I’m not so sure; in fact, I’m downright dubious. After all, the enormously influential International Energy Agency has recommended no new fossil fuel development after 2021 – “no new”, as in zero.

It’s because of pressure such as this that even though U.S. natural gas prices doubled in the fall of 2021 and were still up around 75% over 2020 as the year ended, the natural gas drilling count stayed flat. The last time prices were this high there were three times as many rigs working.

It was the same story with oil production. Most Americans don’t seem to realize it, but the U.S. has provided 90% of the planet’s crude output growth over the past decade. In other words, without America’s extraordinary shale oil production boom — which raised total oil output from around 5 million barrels per day in 2008 to 13 million barrels per day in 2019 — the world long ago would have had an acute shortage. (Excluding the Covid-wracked year of 2020, oil demand grows every year — strictly as a function of the developing world, by the way.)

Unquestionably, U.S. oil companies could substantially increase output, particularly in the Permian Basin, arguably (but not much) the most prolific oil-producing region in the world. However, with the Fed being pressured by Congress to punish banks that lend to any fossil fuel operator, and the overall extreme hostility toward domestic energy producers, why would they?

There is also tremendous pressure from Wall Street on these companies to be ESG compliant. This means reducing their carbon footprint. That’s tough to do while expanding the output of oil and gas. Further, investors, whether on Wall Street or on London’s equivalent, Lombard Street, or pretty much any Western financial center, are against U.S. energy companies increasing production. They would much rather see them buy back stock and pay out lush dividends. The companies are embracing that message. A leading CEO publicly mused to the effect that buying back his own shares at the prevailing extremely depressed valuations was a much better use of capital than drilling for oil.

One U.S. institutional broker reported that of his 400 clients, only one would consider investing in an energy company! Consequently, the fact that the industry is so detested means its shares are stunningly undervalued. How stunningly? Numerous U.S. oil and gas producers are trading at free cash flow yields of 10% to 15% and, in some cases, as high as 25%. (In early 2022, there seems to be a sentiment shift underway. The plethora of pundits who deemed energy “uninvestable” in 2021 are suddenly removing the “un”; it’s amazing what oil prices nearing $100, caused by crashing supplies, does to investor attitudes.)

In Europe, where the same pressures apply, one of its biggest energy companies is generating a 16% free cash flow yield. Moreover, that is based on an estimate of $60 per barrel oil, not the prevailing price of nearly $95, as I apply the final edits to this chapter.

Besides how vital the U.S. shale industry has been to global supplies, another much overlooked fact about shale production is its rapid decline nature. Most oil wells see their production taper off at just 4% or 5% per year. But with shale, that decline rate is 80% after just two years.

As a result, the globe’s most important swing producer, the USA, has to come up with about 1.5 million barrels per day (bpd) of new output just to stay even. Please realize that total U.S. oil production in 2008 was only around 5 million bpd. Thus, 1.5 million barrels per day is a lot of oil and requires considerable drilling and exploration activities. Again, this is merely to stay steady-state, much less grow.

The foregoing is why I wrote on multiple occasions in my newsletter during 2020, when the futures price for oil went below zero, that crude would have a spectacular price recovery later that year, and especially in 2021. Even as it rallied hard throughout most of last year, I continued to opine it had more upside. My repeated 2021 forecast in numerous of our EVAs was that with supply extremely challenged for the above reasons, and demand marching back, I felt we could see $100 crude in 2022, possibly even higher. With it knocking on the triple-digit door in February of this year, that prediction has nearly come to fruition.

Frankly, I believe many in the corridors of power would like to see oil trade that high as it will help catalyze the shift to renewable energy. But consumers are likely to have much different reaction — potentially, a violently different reaction.

You thought 2021’s gas prices were high?

Mike Rothman of Cornerstone Analytics has one of the best oil price forecasting records on Wall Street. Like me, he was vehemently bullish on oil after the Covid crash in the spring of 2020 (admittedly, his well-reasoned optimism was a key factor in my up-beat outlook). Here’s what he wrote in the late summer of 2021: “Our forecast for ’22 looks to see global oil production capacity exhausted late in the year and our balance suggests OPEC (and OPEC + participants) will face pressures to completely remove any quotas.” My expectation is that global supply will likely max out sometime in 2022, barring a powerful negative growth shock, such as a highly virulent and vaccine resistant Covid variant. A significant supply deficit looks inevitable as global demand recovers and exceeds its pre-pandemic level.

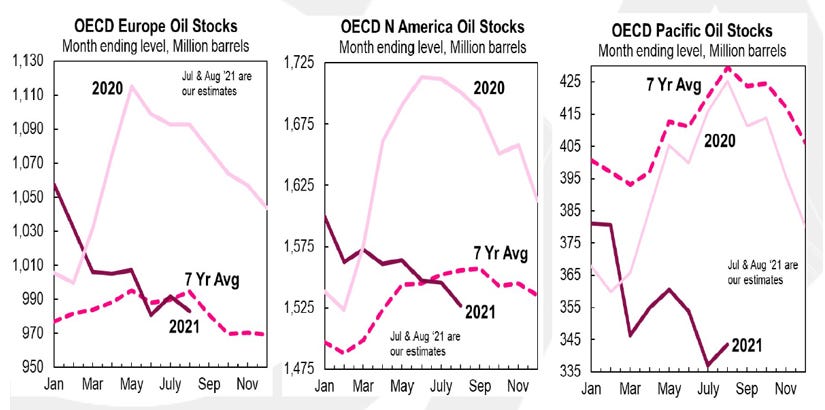

This is a view also shared by Goldman Sachs and Raymond James, among others; hence, my forecast of triple-digit prices next year. Raymond James pointed out that in June of 2021, the oil market was undersupplied by 2.5 mill bpd. Meanwhile, global petroleum demand was rapidly rising with expectations of nearly pre-Covid consumption by year-end. Mike Rothman ran these charts in a webcast on 9/10/2021 revealing how far below the seven-year average oil inventories had fallen. This supply deficit is very likely to become more acute in 2022. (For more on this topic, see the Appendix.)

Figure 2

Source: Mike Rothman

In fact, despite oil prices having already moved over $70 in the early second half of 2021, total U.S. crude volumes were projected to actually decline. This is an unprecedented development. However, as the very pro-renewables Financial Times (the UK’s equivalent of The Wall Street Journal) explained in an August 11th, 2021, article: “Energy companies are in a bind. The old solution would be to invest more in raising gas production. But with most developed countries adopting plans to be ‘net zero’ on carbon emissions by 2050 or earlier, the appetite for throwing billions at long-term gas projects is diminished.”

The author, David Sheppard, went on to opine: “In the oil industry there are those who think a period of plus $100-a-barrel oil is on the horizon, as companies scale back investments in future supplies, while demand is expected to keep rising for most of this decade at a minimum.” (Emphasis mine) To which I say, precisely!

Thus, if he’s right about rising demand, as I believe he is, there is quite a collision looming between that reality and the high probability of long-term constrained supplies. One of the most relevant and fascinating Wall Street research reports I read as I was researching the topic of what I think can be referred to as “Greenflation” was from Morgan Stanley. Its title asked the provocative question: “With 64% of New Cars Now Electric, Why is Norway Still Using so Much Oil?”

While almost two-thirds of Norway’s new vehicle sales are EVs, a remarkable market share gain in just over a decade, in the U.S. the number is an ultra-modest 2%. Yet, per the Morgan Stanley piece, despite this extraordinary push into EVs, oil consumption in Norway has been stubbornly stable.

Coincidentally, that’s been the experience of the overall developed world over the past 10 years, as well: petroleum consumption largely flatlined. Where it hasn’t done an imitation of the EKG of a corpse is in the developing world, which includes China. As you can see from the following Cornerstone Analytics chart, China’s oil demand has vaulted by about 6 million barrels per day (bpd) since 2010 while its domestic crude output has, if anything, slightly contracted.

Figure 3

Source: Cornerstone Analytics

Another coincidence is that this 6 million bpd surge in China’s appetite for oil almost exactly matched the increase in U.S. oil production over the past 12 years. Once again, think where oil prices would be today without America’s shale oil boom.

China’s thirst for oil, as well as the rest of Asia’s, is unlikely to change over the next decade. By 2031, there are an estimated one billion Asian consumers moving up into the middle class. History is clear that higher incomes mean more energy consumption. Unquestionably, renewables will provide much of it, but oil and natural gas are just as unquestionably going to play a critical role. Underscoring that point, despite the exponential growth of renewables over the last 10 years, every fossil fuel category has seen increased usage globally, again, mostly a function of the developing world.

Thus, even if China gets up to Norway’s 64% EV market share of new car sales over the next decade, its oil usage is likely to continue to swell. As you may know, China has become the world’s largest market for EVs — by far. Despite that, the above chart vividly displays an immense increase in oil demand.

Here's a similar factoid that I ran in our December 4th, 2020, EVA, Totally Toxic “(There was) a study by the UN and the US government based on the Model for the Assessment of Greenhouse Gasses Induced Climate Change (MAGICC). It predicted that ‘the complete elimination of all fossil fuels in the US immediately would only restrict any increase in world temperature by less than one-tenth of one degree Celsius by 2050, and by less than one-fifth of one degree Celsius by 2100’. My apologies for asking a politically incorrect question, but if the world’s biggest carbon emitter on a per capita basis causes minimal improvement by going cold turkey on fossil fuels, are we making the right moves by allocating tens of trillions of dollars, that we don’t have, toward the currently in-vogue green energy transition?” Moreover, based on China’s recent no-show at the planet’s main climate change conference (COP 26) in Glasgow in 2021, it seems as though its fondness for fossil fuels isn’t likely to diminish.

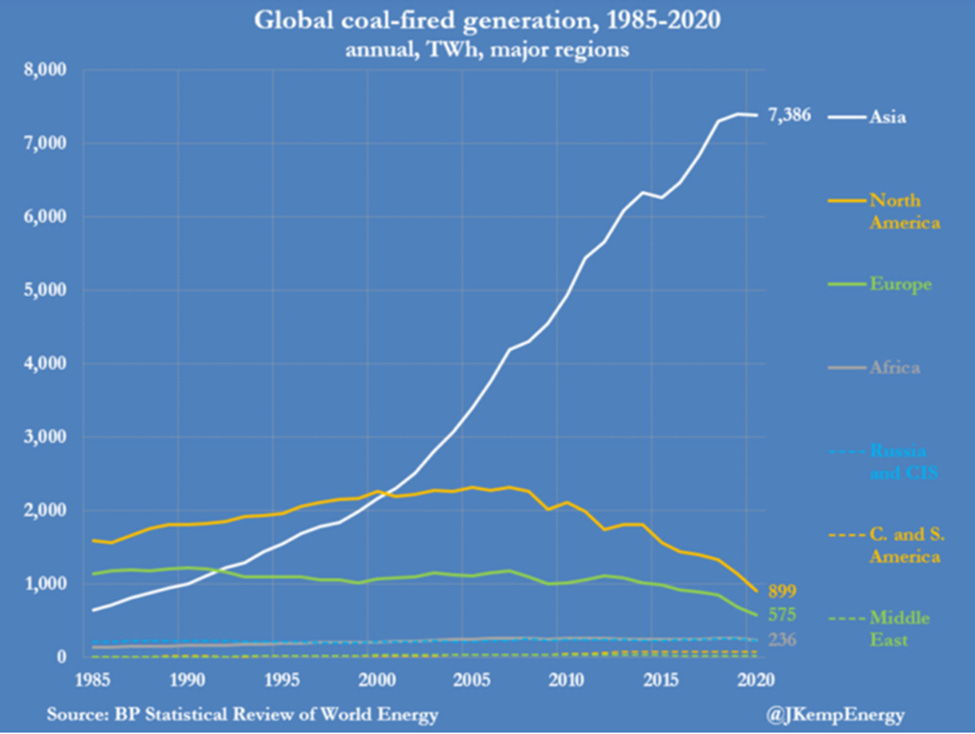

Another reason to expect China’s oil and gas needs to rise in the years ahead is its current heavy reliance on coal. In fact, 70% of China’s electricity is coal generated. Since EVs are charged off a grid that is primarily coal powered, carbon emissions actually rise as the number of such vehicles proliferate. As you can see in the following charts from Reuters’ crack energy expert John Kemp, Asia’s coal-fired generation has risen drastically in the last 20 years, even as it has receded in the rest of the world. (The flattening recently is almost certainly due to Covid, with a sharp upward resumption nearly a given.)

Figure 4

The worst part is that burning coal not only releases CO2 — which is not a pollutant and is essential for life — it also releases vast quantities of nitrous oxide (N20), especially on the scale of coal usage seen in Asia today. N20 is unquestionably a pollutant and a greenhouse gas hundreds of times more potent than CO2. (An interesting footnote is that over the last 550 million years, there have been very few times when the CO2 level has been as low, or lower, than it is today.)

I look forward to part 2 of Green Energy: A Bubble In Unrealistic Expectations. I would hope the rest of the world would pay close attention to China's challenges - and remedies - They know coal cannot work for long and indeed have announced the building of up to 120 nuclear power plants in the country. The US and western Europe would do well to consider this emission-free, reliable source of energy. This should be a "Manhattan Project" priority within national energy policy. Decentralized, small modular plants hold promise. Indeed, Putin's current leverage in waging war with impunity lies in no small part in his control of huge Russian carbon energy supplies that keep Germany, Italy, Hungary and other alive. the more severe sanctions envisioned for Putin and Russia are NOT in play becasue these countries and others fear a severing of their energy sources if they isolate Russia. We can spin turbines and gahter electrons form the sun but not without carbon and energy to build this stuff. Stuff that, by the way, doesn't last for very long...