Meme stocks

This chapter wouldn’t be complete without exploring the memorable meme stock experience seen early in the year. “Meme” refers to those stocks such as AMC Entertainment and GameStop, among others, that appreciated by thousands of percentage points, almost overnight, gravely wounding at least two well-known, and formerly successful, hedge funds.

As most are aware, meme stocks became the playthings of the Robinhood and Reddit investor cohort which numbered in the tens of millions by January 2021. Robinhood, the stock trading platform, not the hero of Sherwood Forest, had 13 million account holders at that point. In the spirit of helping take from the rich to give to the poor, this Robinhood allows free trading to its customers. However, it did receive almost $700 million for selling its “order flow”; i.e., routing its clients’ trades to market-makers such as Citadel Securities, controlled by billionaire Ken Griffin.

In December 2020, Robinhood’s less than altruistic motives were revealed when it was fined $65 million by the SEC for misleading its customers about how much money it made by trafficking in their order flow. This included admitting that it wasn’t diligent about attaining “Best Ex”, or best execution prices. Some experts logically wonder if savvy and opportunistic firms like Citadel are exploiting the knowledge they gain of what amateur investors are buying and selling in order to trade against them and their often irrational moves.

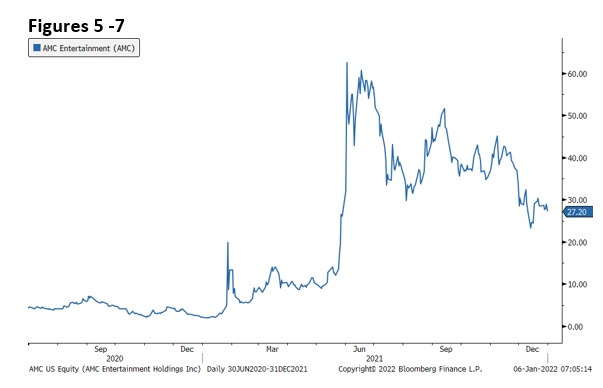

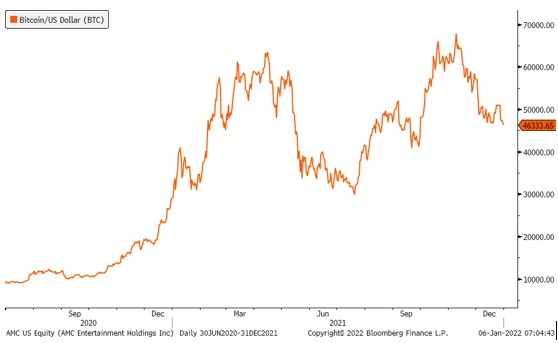

For a time, though, as AMC and GameStop both went vertical — putting to shame even Bitcoin’s 900% rise from its summer of 2020 trough to its spring 2021 high—it looked like the newbies were besting the pros. Actually, it looked more like a beasting than a besting.

Figures 5 - 7

This extraordinary blow off stunned the investing world. Iconoclastic billionaires such as Elon Musk and Mark Cuban egged on the mania, tweeting out such messages: “GameStonk!” (Stonk is Robinhood trader slang for stocks, per the earlier New York magazine cover, particularly the ones its community is embracing.) They were not alone. On January 28th, 2021, The Seattle Times ran the headline “Who’s the ‘dumb money’ now? Day traders lift GameStop to new high.” [i]

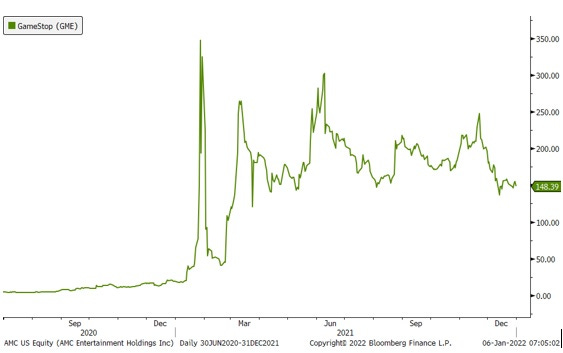

New highs indeed—GameStop (symbol: GME) hit $483 on January 27th, up from $5 in the summer of 2020. The problem was that the role reversal didn’t last long—like 24 hours. On the same day that edition of The Seattle Times landed on the doorstep of the precious few who still receive hard copy papers, GME’s market price was nearly cut in half. By mid-February, it was down to $40. Consequently, all those Robinhooders frantically buying GME as it went postal were nursing horrendous losses. The dumb money once again lived down to its name. (My newsletter did warn about the extreme dangers in meme stocks at the time.)

Speaking of dumb money, passive investing ETFs and index funds, such as those run by BlackRock and Vanguard, were forced to mechanically buy more of these stocks as they went parabolic (or, more accurately, in math jargon, vertically asymptotic — that’s my fancy phrase for this chapter). This is due to the fact that investment vehicles tracking specific indices are required to precisely match something like the Russell 2000 small cap index.

Due to their stunning ascents, GME and AMC became two of the Russell 2000’s largest holdings, regardless of their fundamentally unjustifiable valuations. (When AMC was trading in the 40s in the summer of 2021, the average analyst price target was $5.40, with a high of $16 and a low of $1!) Thus, BlackRock and Vanguard, with their constant inflows of billions upon billions, became two of the largest holders of GME and AMC in 2021. So much for the efficient market theory in action! And perhaps that’s why, by late January 2022, the Russell 2000 Growth Index was approaching a 30% smackdown from its early 2021 peak even as the S&P 500 was still not even in actual correction mode.

Critical to the exponential increases by the meme stocks were “influencers”. Per an August 28, 2021, Wall Street Journal article, the three cardinal rules of influencers were: 1. Be relatable; 2. Sell the dream; 3. All bulls, no bears. Ah, there you have it. As the article’s sub-headline read: “Always be bullish.”

It was an internet influencer by the name of Keith Gill who was the primary instigator behind the GameStop moonshot, and he totally got the always-be-bullish part. In the summer of 2019, a young and obscure Mr. Gill began buying GameStop stock and options. He also started touting his bull case in cyberspace.

Because most millennials were aware that GameStop’s business model was dated and eroding, with online gaming and downloads being where the action was, his bullishness initially drew skepticism from his handful of online followers.

By late 2020, though, GameStop’s price was moving higher, and Mr. Gill began to establish a reputation as a stock market “influencer” on Reddit’s WallStreetBets social media forum. (One of the more popular posts on that is “Buy High, Sell Never”, a meme that is certain to be eventually thoroughly discredited, if it hasn’t been already.)

Outside of this forum, Mr. Gill was largely unknown, until January 2021. From early August 2020 through year-end, GameStop (ticker: GME) rose 500%. But that was just the warm-up act. After rising another 75% in the first two weeks of 2021, to $35, GME began one of the most breathtaking ascents in the history of the financial markets, as shown in Figure 6 above.

By Thursday, January 28th, 2021, when it nearly hit $500, it represented a market capitalization of roughly $32 billion. All for a company that has been profit-free on a cumulative GAAP basis since 2015. (Of course, it never did get as nuts as Dogecoin did; like I said, that one was epic.)

As the first month of 2021 came to a close, GME became the financial market sensation of the young year. It attracted scrutiny from key members of Congress, along with causing tremendous stress for Robinhood’s trading platform upon which much of the GME buying frenzy occurred. To cope with the regulatory capital requirements of the spectacular volume explosion, it was forced to raise $3 billion almost overnight. Briefly, Robinhood, TD Ameritrade, and Charles Schwab suspended transactions of GME, attracting considerable criticism, with Robinhood taking the brunt of the blowback.

Supposedly, there were more GME shares sold short than were outstanding, a remarkable development that begs the question of how regulators allowed that to happen. Curiously, the SEC was largely missing in action as the GME phenomenon unfolded (other than a terse message in late January 2021 that markets should be allowed to function). Similarly, the Fed did nothing to intervene, such as to raise margin requirements. Years back, when the Fed sought to interdict bubbles — rather than enable them — it frequently increased the amount of capital investors needed to put up to buy stocks when conditions became highly speculative and/or volatile.

In case you’re bemused as to how a rag-tag informal army of online traders like Mr. Gill — whose rallying cry is YOLO (You Only Live Once) — can overwhelm multi-billion-dollar hedge funds, it is due to a confluence of factors. First, many, if not most, of these players (and for many of them it truly is a game) use margin debt, often combined with options. Thus, they can control far more market value than they actually put up in cash.

To maximize their option leverage, they often purchase far-out-of-the money calls (meaning, the right-to-buy, or exercise, price is way above the current stock price; thus, they can be bought for chump change with lottery-like payoffs in the case of a GME-type move). As the swarm of call options (bullish bets on the underlying stock) swells, option market-makers are forced to buy the underlying shares to hedge their de facto short option positions.

This buying naturally further reinforces the shares’ upward trajectory which, in turn, creates even more of a feeding frenzy among buyers — particularly when they smell short sellers’ blood in the water. One pundit appropriately referred to this as the “weaponization” of call options.

Second, the “Reddit Rebels” often move in concert, egging each other on with frequently obscene and boastful verbiage. Screenshots of their brokerage accounts show multi-million-dollar gains, inciting intense greed and FOMO (Fear Of Missing Out.) Influencers like Mr. Gill are shrewd enough to target stocks such as GME with high short positions. As the shorts take huge hits, often triggering margin calls, the share price typically goes straight up. Any connection to true intrinsic value is severed and, for a time anyway, becomes totally meaningless.

Third, social media platforms like Facebook, Twitter and YouTube use algorithms and, as we should all know, these select the most compelling content based on past user activity. These “algos” then push fresh material along similar lines to countless other interested parties. As a result, a powerful digital amplification process occurs, accentuating the hysteria in the case of short squeezes. The Wall Street Journal’s Christopher Mims wrote about this phenomenon during the height of meme madness: “Ample research has described the addictive potential of social media and apps like Robinhood, which make trading stocks feel like gambling… drop them into a stew of sensation-seeking young people with limited entertainment options during a pandemic, and it’s hardly surprising that all of this has come to pass.”

In such situations, short sellers, like the unfortunate hedge funds I mentioned earlier, become trapped by wave upon wave of leveraged, self-reinforcing buying. They learn the hard way about the old market adage that: “He who sells what isn’t hissen’, buys it back or goes to prison.” These days, it’s either put up (as in cash to meet the margin calls) or get sold out.

As I was writing these words in the fall of 2021, GME and AMC, the signature meme stocks, have gone through multiple cycles of breathtaking run-ups and nauseating bungee dives. However, the Himalayan heights they hit in January and June 2021, respectively, have not been retaken. At this point, they appear to be in a long, jagged return to terra firma and their legions of FOMO/YOLO traders seem to have increasingly lost interest in them. As numerous media reports indicated, many (most?) of them have lost considerable sums of money, too.

Of course, the influencers, like Mr. Gill, likely made a killing. When he reportedly liquidated his position in GME, he was alleged to have accrued $20 million in gains on it. Who said “pump and dump” was illegal? (For a compilation of other absurdities, please see the Appendix.)

Because cryptos, SPACs, NFTs, and meme stocks were extreme, and ironic, beneficiaries of the pandemic investing environment, they have been the ultimate examples of what I believe is the greatest wealth destroyer known to woman or man: the moonshot move, i.e., an asset or asset class, like cryptos, that goes parabolic. As I discuss in other parts of this book — but this chapter is most relevant to the topic — a major contributor to the problem is the intense media attention these straight-up spikes receive. The media frenzy stokes a nearly irresistible allure of seemingly instant and easy money. Essentially, these lottery-like payoffs, that seemed to be happening continually in 2021, aroused one of our worst human emotions: unadulterated greed. (Please see the end of the Appendix for this chapter to read a short recap of one of the highest profile examples of this phenomenon.)

These manias are in a way metaphors for the new American meme, to borrow that term, which has, in many ways, replaced the old America dream: The idea that money, success, prosperity, fame, early retirement, to be another Kevin Gill and have all of the above, whatever is your ultimate dream scenario, can be attained nearly overnight and without the typical extreme effort, like Gladwell’s oft-cited 10,000-Hour Rule.

Maybe today it’s the Fed’s ten trillion (almost) rule. If it can magically whip up trillions of fake money, why try to succeed the old-fashioned way? We’ve moved to the polar opposite of those ancient John Houseman Smith Barney ads: “They earn it!” Rather these days, it seems as though with outfits such as Robinhood it's more like “We churn it!” It wins — and Citadel wins even more — but the millions of social media market warriors who trade through them and fell for the get-rich-quick siren song, end up wiped out and even angrier than they were before they were infected with meme madness.

It’s the “something for nothing” mindset and I believe the Fed has enabled that attitude. The eight trillion it has generated literally just from its computer banks has reverberated and been amplified not only through financial markets but through much of American society. We’ve been led to believe, particularly through MMT — which, in my mind, unquestionably produced the insanity bubble — that fake money can produce real and lasting prosperity. Again, to me, nothing could be further from the truth. This has been a massive fake-out and millions have fallen for it.

To end this chapter on the modern-day madness of crowds, I thought this anecdote was an ideal capstone: Someone very lucky, or very smart, bought $8000 of a Dogecoin knockoff known as Shiba Inu (SHIB) in August of 2020. It was worth $5.7 billion 13 months later! Somehow, being a billionaire just isn’t quite as exclusive as it used to be. In my mind, the eventual post-mortem of this biggest bubble ever is almost certain to conclude along the lines of: “How could so many have been so stupid?” Except, of course, for those rare individuals savvy enough to sell into the insanity.

[i] Around this time, one of the highest profile influencers, Dave (Davey Day Trader) Portnoy tweeted: “I’m sure Warren Buffett is a great guy but when it comes to stocks he’s washed up. I’m the captain now.”. Increasingly, it’s looking like Captain Davey is going down with his ship and his crew of similarly hubristic day traders. Meanwhile, Mr. Buffett’s Berkshire Hathaway stock recently hit an all-time high.