The Insanity Bubble

The Insanity Bubble

Chapter 10, Complete

The bubble to end all bubbles

In my admittedly totally biased opinion, I believe this is one of the most important chapters of this book, if not THE most important. That’s because it pulls together an abundance of evidence on the sheer lunacy that commandeered America’s investing mindset in 2020 and 2021. If you were to suggest friends and family read just one chapter in this book, I’d recommend it for that purpose.

Harking back to Chapter 5 on Modern Monetary Theory (MMT), if America was truly practicing that controversial economic system in the early part of the 2020s, one would expect the nearly limitless liquidity MMT provides to show up in wildly speculative investor behavior. Was there any tangible evidence of that as 2021 was winding down? Maybe just a little…

Perhaps a reasonable way to start this chapter is to reflect on words uttered by former Fed chairman Alan Greenspan way back in late summer of 2002, when he was still venerated as “The Maestro” and the erstwhile tech bubble had blown itself to bits. To wit: “Bubbles are often precipitated by perceptions of real improvements in the productivity and underlying profitability of the corporate economy. But as history attests, investors then too often exaggerate the extent of the improvement in economic fundamentals. Human psychology being what it is, bubbles tend to feed on themselves, and booms in their later stages are often supported by implausible projections of potential demand. Stock prices and equity premiums are then driven to unsustainable levels. Certainly, a bubble cannot persist indefinitely.” (Emphasis mine)

Speaking of “certainly”, it certainly would have been more helpful to millions of investors if he had delivered these cautionary words three years earlier when the internet and dotcom mania of that era was still raging. Regardless, the wisdom of his utterances was well worth reflecting upon in the early years of the roaring 2020s because, in my opinion, the degree of speculation since Covid struck has, ironically, exceeded what was seen in the late 1990s. In Chapter 14, I will focus on the overall U.S. stock market, but for now let’s examine what is going on within some of the most casino-like realms of asset markets (using the word “asset” very loosely). These are where the quaint notions that Mr. Greenspan was referring to like “productivity”, “profitability” and “economic fundamentals” are total non-issues.

The below April 2021 cover from New York Magazine succinctly captures the prevailing zeitgeist of this era, the “new world of money”, as it refers to it, that I will chronicle below. It’s definitely a very brave new world... if not an utterly reckless one.

Figure 1

Cryptos

One of the most salient examples of the lack of economic factors is in the chaotic world of crypto currencies. Of course, there are no earnings, dividends, or profits (other than by trading them) that underlie the cryptos. This is not to disparage Bitcoin and Ethereum, which do have unique attributes in terms of growing acceptance by businesses and institutional investors alike. They also offer scarcity due to a limited amount of future supply. Further, there’s little doubt the blockchain technology that authenticates and facilitates transactions in them is here to stay.

However, the scarcity appeal of Bitcoin (which has a hard cap of 21 million units to be “mined” or created) doesn’t extend to the crypto space in general. As of early 2022, there are roughly 6000 different cryptos with more being created on a regular basis. Undoubtedly, there is a plethora of examples of the prevailing insanity in cryptos presently, but there is one in particular that, to me, perfectly captures the mood of the moment.

While there has been a lot of shameless promoting of various cryptos by their creators and paid floggers — often with the express intent of the insiders selling into the buying frenzy they whip up — that accusation cannot be leveled at Billy Markus, the co-founder of Dogecoin. In early 2021, Mr. Markus told The Wall Street Journal that: “The idea of Dogecoin being worth 8 cents is the same as GameStop being worth $325.” (We’ll get to that one later in this chapter.) “It doesn’t make sense. It’s super absurd. The coin design was absurd.” Perhaps what Mr. Markus was missing with his candid observations is that an exhaustive list of markets has become theaters of the absurd. But the theatrics of Dogecoin are definitely hard to top.

Though it was already up from half a penny per coin at the end of 2020 to the aforementioned 8 cents, amounting to a market value of $10 billion when he expressed his incredulity, it was ultimately heading to 64 cents for an $80 billion market cap (capitalization, i.e., the number of coins outstanding times market price) by May of 2021. This for something that, per its creator, was not just absurd, but super-absurd. As the Journal ironically noted, referring to Mr. Markus: “He set out to create a coin so ridiculous it could never be taken seriously.” Incredibly, there were blue chip companies with strong franchises, healthy dividends and growing profits that were trading for less than $80 billion during 2021. This was despite the fact that the U.S. stock market was trading at one of its priciest levels ever by multiple metrics. (Again, more on that topic in Chapter 14.)

One reason why Mr. Markus argued against his own brainchild’s worth was that he intentionally designed it to have unlimited supply, in contrast to Bitcoin, with its 21-million maximum. Why would rational investors pay as much as $80 billion for an alleged asset that could be produced in limitless quantities? (If you’re similarly wondering why people around the world value U.S. dollars so highly when the Fed is fabricating them in seemingly infinite amounts, you won’t get an argument from me.)

Despite its inherent worthlessness, Dogecoin’s extraordinary market success has brought about the sincerest form of flattery. By 2021’s third quarter, there were nearly 100 cryptocurrency tokens that included “doge” in their name.[i]

Beyond dodgy Dogecoin and the thousands of likely value-free cryptos floating around, there is also the issue of the so-called “stable” coins. (In my mind, due to their questionable long-term viability and fiction of stability a better name might be “fable” coins.) Tether is the dominant stable coin and is used for most crypto transactions, including Bitcoin. Thanks to my great friend and fellow newsletter author extraordinaire, Grant Williams, I came to believe in the summer of 2021 that Tether is a fraud. That’s a strong word, and it deserves some serious backing up… which is exactly what I’ll now do.

In case you don’t know, a stable coin is supposed to be backed one-to-one with something like U.S. treasuries or other ultra-safe assets. For years, Tether insisted that was true in its case. Unfortunately for the planet’s leading stable coin, New York State Attorney General, Letitia James, begged to differ.

Moreover, it’s my strong suspicion that either the U.S. Department of Justice, or the SEC (or both) are on the verge of untethering it once and for all. In fact, not long after I ran some of my Tether text in our July 23rd, 2021, EVA, Bloomberg announced that criminal indictments against its senior management were being prepared. (However, as I write these words, no actual indictment has occurred.)

Despite Tether’s protestations of its innocence, the New York Attorney General’s office secured an $18-million-dollar fine against it as well as its incestuously related firm, Bitfinex. Further, it banned both from conducting business in the state of New York. Sadly, that leaves the other 49 states, and millions of gullible crypto investors in them, at the mercy of this demonic duo, not to mention the rest of the world.

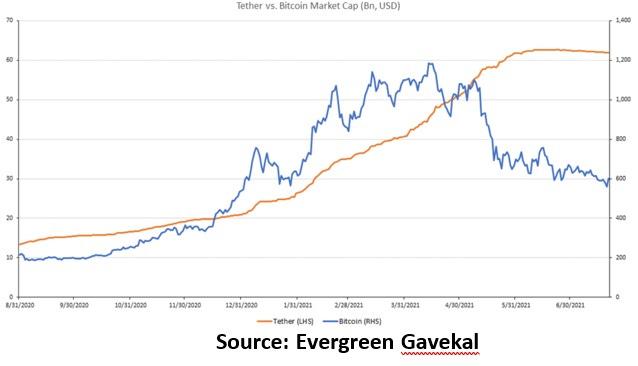

As you can see in the following chart, there was a remarkable correlation between the rise in the number of Tethers outstanding and the 900% moonshot by Bitcoin from the summer of 2020 until the spring of 2021. This pushed the world’s leading crypto to a mind-bending $1 trillion. Further, once the quantity of Tethers flatlined, Bitcoin entered a nasty correction, before another frenzied rally ensued, followed by a 40% faceplant from November 2021 to early January 2022 (as of late January, its decline was approaching 50%).

Figure 2

Even a casual observer might wonder if there wasn’t a causal relationship. In my mind, Tether going from around $12 billion worth of coins outstanding (remember, these are supposed to be backed one-to-one by real assets) to $64 billion is closely linked to Bitcoin ripping by 450% at the same time.

Skeptics about this linkage would point out that even Bitcoin’s starting value last fall of roughly $150 billion would be tough to move — certainly, all the way to $1 trillion — with just $60 billion of Tether (not all of which went into Bitcoin, by the way). However, this ignores two things: first, only about 20% of Bitcoin is estimated, on the high side, to actually trade; second, prices are set by the marginal transaction which is, even for U.S. large cap stocks, usually just a tiny fraction of the total market value.

Thus, $60 billion of fresh “capital” coming in can have a huge impact, particularly if there is a lot of leverage involved which, in the case of Tether and Bitcoin, is a given. (For a summary of an eye-opening, jaw-dropping and head-shaking podcast Grant did with two forensic investigators on the Tether situation in the summer of 2021, see the Chapter 10 Appendix)

Many crypto fans concede that Tether smells bad. But their common rationalization is that it really doesn’t matter to Bitcoin and the other digital “currencies”. Some even think Bitcoin would go up as money flows from Tether into Bitcoin directly, should the leading fable-, sorry, stable-coin implode.

They might be right but, again, I don’t think that’s what the odds favor. Because so much funding of cryptos has been via Tether and other “stable coins”, anything causing millions of investors to question their backing would seem to me to be a cataclysmic event in crypto space.

The crypto exchanges like Coinbase also would almost certainly come under intense pressure due to any broad crisis of confidence. Even some ardent crypto fans are advising investors to extract coins from the crypto exchanges to avoid what could essentially be a run on them.

If I’m right about this, there could be an exceptional buying opportunity in Bitcoin and possibly Ethereum as they should ultimately benefit from the collapse of the plethora of shitcoins. (Sorry for the vulgarity but it’s just so appropriate!)

Here’s one fascinating factoid to end this section on: during the Covid crisis, the market value of all cryptos was $154 billion. By March of 2021, it was $1.75 trillion. Astounding, yes, but not the ultimate shocker — four months later that number was $3 trillion. And yet our precious central bank is still afraid to utter the “B” word!

NFTs

Moving on from cryptos, let’s examine another one of the truly bizarre manifestations of Bubble 3.0 and the tens of trillions of global central bank funny money – NFTs. For my more “mature” (and conservative) readers, this stands for Non-Fungible Tokens. That helps a lot, right?

Maybe a peak into the art world might help convey (sort of) what these things are. To quote Barron’s on those that are art-related: “NFTs are unique digital works encrypted with an artist’s signature that prove authenticity and ownership.” The artist Beeple discovered the joys of NFTs in March 2021 when a digital collage of his creations, “Everydays: The First 5000 Days”, sold for $69 million. It had been minted as a digital token and stored on blockchain (the previously mentioned cyber-ledger widely used for crypto trading).

While Beeple’s NFT was certainly the blockbuster, it wasn’t a fluke. There was subsequently a string of million-dollar-plus NFT transactions. One involved Twitter founder Jack Dorsey’s first tweet, which fetched nearly $3 million in March of 2021. Showing how mainstream NFTs had gone by 2021, Barron’s ran this cover story on them in their Penta special supplement, oriented toward the high-net-worth set.

Consider these illuminating comments by Evan Beard, national art services director at BofA’s Private Bank in Barron’s Penta. First, he noted the advantages, and then just a bit of a problem. “Art gives you utility and NFTs have been lacking in the utility delivered to the client—in the aesthetic value, the pleasure, the status.” Then, the not-so-hot news: “We believe 99.9% of NFTs being minted right now will go to zero.” That seems a bit extreme to me but in the approximate disastrous neighborhood (and reminiscent of what is probably in store for almost all those 6000 or so cryptocurrencies).

On a much more mundane, but quite humorous, level, Charmin, (yes, the maker of the cotton-ball soft TP), auctioned rolls of its signature product accompanied by some artistic designs. It immediately received a bid for $2100. Personally, I’d rather buy mine at Costco and they can keep the art.

In another crypto echo, NFT artists can generate one design and then replicate it 10,000 times. Call me old-fashioned but I don’t think that has the makings of a scarce investment. The venerable bubble-buster Jim Grant cited the example of an NFT series by some outfit called EtherRocks. With eerie resemblance to Dogecoin, one fan referred to its NFT collection accordingly: “It’s so stupid that it’s perfect.” Forrest Gump might have quipped about how: “Stupid is as stupid does.” And someone did something incredibly stupid, at least in my mind, with another NFT called the Bored Ape Yacht Club. Per Mr. Grant, a pair of their tokens, along with a warrant (like an option) to create new ape variants, went for a cool $26.2 million at a Sotheby’s auction in September 2021. The buyer clearly went ape… sorry, I won’t use another four-letter word.

Again, quoting Grant’s Interest Rate Observer (IRO), one of my favorite research reads, “Some vendors offer images to which they have no rightful claim.” That seems like a problem, but maybe I’m being picky.

EtherRocks’ website, once more courtesy of Grant’s IRO, also channels Dogecoin’s Markus by advising that its assets: “…serve NO PURPOSE beyond being able to be brought (sic) and sold.” Maybe it wasn’t a sloppy typo; perhaps it meant bring it and we’ll sell it — no questions asked. Somehow, I strongly suspect EtherRocks takes a cut of the transactions it processes.

EtherRocks also managed to pay homage to its name by cleverly resuscitating the 1970s pet rock rage. Several of these sold for $100,000, or more, in the summer of 2021. The first half of 2021 turned out to be a golden age for NFTs with $2.5 billion in transaction volume (realizing this pales in comparison to cryptos).

But the much bigger NFT money involves CryptoPunks (if you’ve heard of it, I’m impressed; or worried about where you spend your spare time… and investment dollars). According to Wikipedia, each one has been algorithmically produced via computer code. Allegedly, no two images are precisely alike, but some have more unusual characteristics than others. They were originally free and could be acquired by anyone with an Ethereum wallet.

Like Bitcoin, they have a hard issuance cap. In this case, it is far lower at 10,000. 1000 of those existing images are shown below. Apparently, most of these images are of humans but there is also a smattering of Zombies, Apes (it seems as though the NFT world is “Planet of the Apes”) and Aliens. It’s nice to know humanity keeps such good company.

Figure 4

But don’t laugh — a CryptoPunk that was purchased for $443 in 2018 sold for almost $4.4 million, at least in Ethereum (which is theoretically convertible into US dollars). And all of you crypto traders reading this thought you were crushing it with Bitcoin!

SPACs

The craziness doesn’t end with NFTs, of course. There is another acronym that is in some ways yet more outrageous, if nothing else for the large sums involved. This initialism is SPAC and it stands for Special Purpose Acquisition Company. SPACs are basically so-called “blank check” entities. They are funded by investors who are willing to trust that the SPAC will make wise investments with the capital they raise. Typically, the actual investment is unknown at the time of funding, hence the blank check nomenclature.

SPACs became enormously popular in 2021 despite their opacity. In the first quarter alone, SPACs represented $170 billion in mergers and acquisitions, commonly known as M&A, amounting to roughly 25% of all M&A activity.

SPACs themselves raised nearly $80 billion in fresh capital in 2021’s first three months, slightly more than for all of 2020, almost totally on U.S. exchanges (befitting America’s status as the world’s most overvalued and wildly speculative investment venue). This early year hyper-popularity caused me to warn in my January 1st, 2021 EVA that SPACs were due for a serious spanking. Since that time, the SPAC ETF (of course, there’s an ETF for them!) swooned by 35%, even though the S&P 500 has vaulted roughly 20%.

Trusting in SPAC sponsors to intelligently and carefully deploy capital in an environment where almost everything has been driven up to ridiculous valuations by trillions of central bank liquidity creation is another remarkable leap of faith. The SPAC insiders have a great deal: If they get lucky and their SPAC explodes higher — as many have done, often before imploding — they make a killing; if it flops, they still make good returns due to their rewards for establishing the SPAC. Thus, their incentive is to launch these deals and hope they find a solid investment… or, more likely, a sexy story that they can spin to push up the market price. This allows them to sell at least a portion of their ownership interest that they typically received at no cost.

Starwood CEO Barry Sternlicht had this to say about SPACs during the heady days of their amazing craze: “You can’t compete against stupidity. It’s a little out of control. No, it’s a lot out of control. Don’t expect Wall Street to regulate the launch of SPACs. They’re making too much money. If you can walk, you can do a SPAC.” As the old Wall Street idiom goes: When the ducks are quacking, feed them.

90-year-old Sandy Robertson built his investment career as a stockbroker helping Warren Buffett accumulate a 5% stake in American Express in the early 1960s, when that iconic U.S. company’s stock had been pummeled. (For an interesting nugget of Buffettology, please refer to the Appendix.) Sandy went on to become one of Silicon Valley’s earliest and most renowned dealmakers, helping to co-found two of the Valley’s leading investment firms: the eponymous Robertson Stephens and Montgomery Securities. Thus, he’s seen his share of bubbles and busts.

When SPAC mania was still raging in the first half of 2021, he told The Financial Times: “This SPAC thing is very indicative of the later stages of a cycle.” (He could have also said “bubble” instead of “cycle”.) “There are some that are pretty good, but at the bottom there is a lot of junk.” (He could have also used another four-letter word that would be much stronger than “junk”.)

After noting that there were far too many buyers chasing after a limited amount of worthwhile takeover targets, he went on to say: “The seller has the advantage on the price. They (the SPACs) are going to pay too much. It’s the proliferation of them that I’m worried about.” He was alluding to the fact that SPACs have a limited time to make their play; otherwise, they need to return the uncommitted funds back to investors, a most unlucrative outcome for the sponsors. Thus, they are in a hurry to find targets and rushing is a recipe for making imprudent investments. Based on how hard these have been hit since their early 2021 apex, Mr. Robertson’s warnings were well founded.

Before moving ahead to the next example of 2021’s casino conditions, I’ll end this section with one of the most incredible case studies in SPAC absurdity. A SPAC by the name of Hometown International managed to raise $2.5 million, including from the universities of Duke and Vanderbilt. Perhaps that sounds like a modest amount, but its market value was anything but in May of 2021 when it hit $100 million. What was truly modest was the SPAC’s lone asset (other than its rapidly depleting cash): a delicatessen in Paulsboro, New Jersey. This was not exactly the second coming of Carnegie Deli; it’s total sales in 2020 were $13,976. That’s right—no zeroes after the number.

Hometown International’s CEO also serves as the wrestling coach at the local high school. He grandly told The Financial Times that: “We will not restrict our potential candidate target companies to any specific business, industry, or geographical location.” Perhaps a wrestling coach’s skills are exactly what’s needed for a tiny deli to do a takedown of a much larger entity… which would be just about any company.

As Columbia law professor and takeover expert John Coffee told the FT, referring to Hometown International, sounding a lot like Sandy Robertson: “(It) is a self-parody of a SPAC. And that’s what I would expect at the end of a bubble.” Hedge fund legend David Einhorn, marveling at this monstrous disconnect between true value and market value—even by 2021’s outrageous standards—quipped: “The pastrami must be amazing.”

Meme stocks

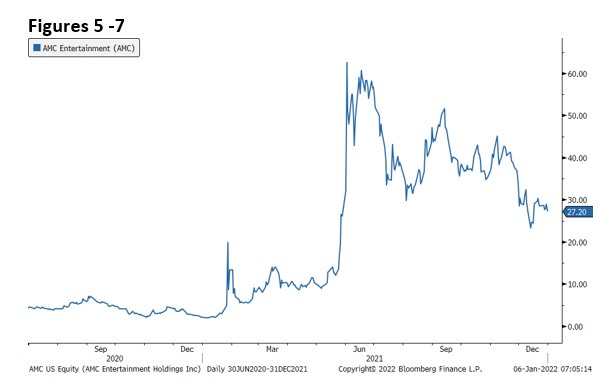

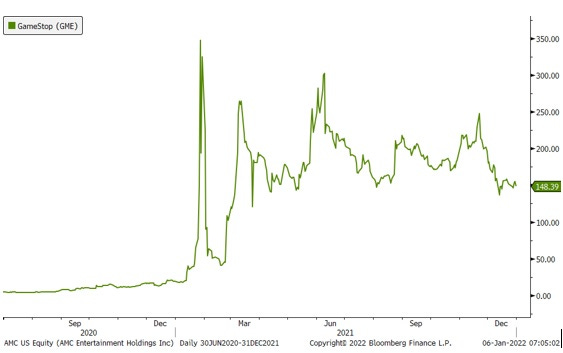

This chapter wouldn’t be complete without exploring the memorable meme stock experience seen early in the year. “Meme” refers to those stocks such as AMC Entertainment and GameStop, among others, that appreciated by thousands of percentage points, almost overnight, gravely wounding at least two well-known, and formerly successful, hedge funds.

As most are aware, meme stocks became the playthings of the Robinhood and Reddit investor cohort which numbered in the tens of millions by January 2021. Robinhood, the stock trading platform, not the hero of Sherwood Forest, had 13 million account holders at that point. In the spirit of helping take from the rich to give to the poor, this Robinhood allows free trading to its customers. However, it did receive almost $700 million for selling its “order flow”; i.e., routing its clients’ trades to market-makers such as Citadel Securities, controlled by billionaire Ken Griffin.

In December 2020, Robinhood’s less than altruistic motives were revealed when it was fined $65 million by the SEC for misleading its customers about how much money it made by trafficking in their order flow. This included admitting that it wasn’t diligent about attaining “Best Ex”, or best execution prices. Some experts logically wonder if savvy and opportunistic firms like Citadel are exploiting the knowledge they gain of what amateur investors are buying and selling in order to trade against them and their often irrational moves.

For a time, though, as AMC and GameStop both went vertical — putting to shame even Bitcoin’s 900% rise from its summer of 2020 trough to its spring 2021 high—it looked like the newbies were besting the pros. Actually, it looked more like a beasting than a besting.

Figures 5 - 7

This extraordinary blow off stunned the investing world. Iconoclastic billionaires such as Elon Musk and Mark Cuban egged on the mania, tweeting out such messages: “GameStonk!” (Stonk is Robinhood trader slang for stocks, per the earlier New York magazine cover, particularly the ones its community is embracing.) They were not alone. On January 28th, 2021, The Seattle Times ran the headline “Who’s the ‘dumb money’ now? Day traders lift GameStop to new high.” [ii]

New highs indeed—GameStop (symbol: GME) hit $483 on January 27th, up from $5 in the summer of 2020. The problem was that the role reversal didn’t last long—like 24 hours. On the same day that edition of The Seattle Times landed on the doorstep of the precious few who still receive hard copy papers, GME’s market price was nearly cut in half. By mid-February, it was down to $40. Consequently, all those Robinhooders frantically buying GME as it went postal were nursing horrendous losses. The dumb money once again lived down to its name. (My newsletter did warn about the extreme dangers in meme stocks at the time.)

Speaking of dumb money, passive investing ETFs and index funds, such as those run by BlackRock and Vanguard, were forced to mechanically buy more of these stocks as they went parabolic (or, more accurately, in math jargon, vertically asymptotic — that’s my fancy phrase for this chapter). This is due to the fact that investment vehicles tracking specific indices are required to precisely match something like the Russell 2000 small cap index.

Due to their stunning ascents, GME and AMC became two of the Russell 2000’s largest holdings, regardless of their fundamentally unjustifiable valuations. (When AMC was trading in the 40s in the summer of 2021, the average analyst price target was $5.40, with a high of $16 and a low of $1!) Thus, BlackRock and Vanguard, with their constant inflows of billions upon billions, became two of the largest holders of GME and AMC in 2021. So much for the efficient market theory in action! And perhaps that’s why, by late January 2022, the Russell 2000 Growth Index was approaching a 30% smackdown from its early 2021 peak even as the S&P 500 was still not even in actual correction mode.

Critical to the exponential increases by the meme stocks were “influencers”. Per an August 28, 2021, Wall Street Journal article, the three cardinal rules of influencers were: 1. Be relatable; 2. Sell the dream; 3. All bulls, no bears. Ah, there you have it. As the article’s sub-headline read: “Always be bullish.”

It was an internet influencer by the name of Keith Gill who was the primary instigator behind the GameStop moonshot, and he totally got the always-be-bullish part. In the summer of 2019, a young and obscure Mr. Gill began buying GameStop stock and options. He also started touting his bull case in cyberspace.

Because most millennials were aware that GameStop’s business model was dated and eroding, with online gaming and downloads being where the action was, his bullishness initially drew skepticism from his handful of online followers.

By late 2020, though, GameStop’s price was moving higher, and Mr. Gill began to establish a reputation as a stock market “influencer” on Reddit’s WallStreetBets social media forum. (One of the more popular posts on that is “Buy High, Sell Never”, a meme that is certain to be eventually thoroughly discredited, if it hasn’t been already.)

Outside of this forum, Mr. Gill was largely unknown, until January 2021. From early August 2020 through year-end, GameStop (ticker: GME) rose 500%. But that was just the warm-up act. After rising another 75% in the first two weeks of 2021, to $35, GME began one of the most breathtaking ascents in the history of the financial markets, as shown in Figure 6 above.

By Thursday, January 28th, 2021, when it nearly hit $500, it represented a market capitalization of roughly $32 billion. All for a company that has been profit-free on a cumulative GAAP basis since 2015. (Of course, it never did get as nuts as Dogecoin did; like I said, that one was epic.)

As the first month of 2021 came to a close, GME became the financial market sensation of the young year. It attracted scrutiny from key members of Congress, along with causing tremendous stress for Robinhood’s trading platform upon which much of the GME buying frenzy occurred. To cope with the regulatory capital requirements of the spectacular volume explosion, it was forced to raise $3 billion almost overnight. Briefly, Robinhood, TD Ameritrade, and Charles Schwab suspended transactions of GME, attracting considerable criticism, with Robinhood taking the brunt of the blowback.

Supposedly, there were more GME shares sold short than were outstanding, a remarkable development that begs the question of how regulators allowed that to happen. Curiously, the SEC was largely missing in action as the GME phenomenon unfolded (other than a terse message in late January 2021 that markets should be allowed to function). Similarly, the Fed did nothing to intervene, such as to raise margin requirements. Years back, when the Fed sought to interdict bubbles — rather than enable them — it frequently increased the amount of capital investors needed to put up to buy stocks when conditions became highly speculative and/or volatile.

In case you’re bemused as to how a rag-tag informal army of online traders like Mr. Gill — whose rallying cry is YOLO (You Only Live Once) — can overwhelm multi-billion-dollar hedge funds, it is due to a confluence of factors. First, many, if not most, of these players (and for many of them it truly is a game) use margin debt, often combined with options. Thus, they can control far more market value than they actually put up in cash.

To maximize their option leverage, they often purchase far-out-of-the money calls (meaning, the right-to-buy, or exercise, price is way above the current stock price; thus, they can be bought for chump change with lottery-like payoffs in the case of a GME-type move). As the swarm of call options (bullish bets on the underlying stock) swells, option market-makers are forced to buy the underlying shares to hedge their de facto short option positions.

This buying naturally further reinforces the shares’ upward trajectory which, in turn, creates even more of a feeding frenzy among buyers — particularly when they smell short sellers’ blood in the water. One pundit appropriately referred to this as the “weaponization” of call options.

Second, the “Reddit Rebels” often move in concert, egging each other on with frequently obscene and boastful verbiage. Screenshots of their brokerage accounts show multi-million-dollar gains, inciting intense greed and FOMO (Fear Of Missing Out.) Influencers like Mr. Gill are shrewd enough to target stocks such as GME with high short positions. As the shorts take huge hits, often triggering margin calls, the share price typically goes straight up. Any connection to true intrinsic value is severed and, for a time anyway, becomes totally meaningless.

Third, social media platforms like Facebook, Twitter and YouTube use algorithms and, as we should all know, these select the most compelling content based on past user activity. These “algos” then push fresh material along similar lines to countless other interested parties. As a result, a powerful digital amplification process occurs, accentuating the hysteria in the case of short squeezes. The Wall Street Journal’s Christopher Mims wrote about this phenomenon during the height of meme madness: “Ample research has described the addictive potential of social media and apps like Robinhood, which make trading stocks feel like gambling… drop them into a stew of sensation-seeking young people with limited entertainment options during a pandemic, and it’s hardly surprising that all of this has come to pass.”

In such situations, short sellers, like the unfortunate hedge funds I mentioned earlier, become trapped by wave upon wave of leveraged, self-reinforcing buying. They learn the hard way about the old market adage that: “He who sells what isn’t hissen’, buys it back or goes to prison.” These days, it’s either put up (as in cash to meet the margin calls) or get sold out.

As I was writing these words in the fall of 2021, GME and AMC, the signature meme stocks, have gone through multiple cycles of breathtaking run-ups and nauseating bungee dives. However, the Himalayan heights they hit in January and June 2021, respectively, have not been retaken. At this point, they appear to be in a long, jagged return to terra firma and their legions of FOMO/YOLO traders seem to have increasingly lost interest in them. As numerous media reports indicated, many (most?) of them have lost considerable sums of money, too.

Of course, the influencers, like Mr. Gill, likely made a killing. When he reportedly liquidated his position in GME, he was alleged to have accrued $20 million in gains on it. Who said “pump and dump” was illegal? (For a compilation of other absurdities, please see the Appendix.)

Because cryptos, SPACs, NFTs, and meme stocks were extreme, and ironic, beneficiaries of the pandemic investing environment, they have been the ultimate examples of what I believe is the greatest wealth destroyer known to woman or man: the moonshot move, i.e., an asset or asset class, like cryptos, that goes parabolic. As I discuss in other parts of this book — but this chapter is most relevant to the topic — a major contributor to the problem is the intense media attention these straight-up spikes receive. The media frenzy stokes a nearly irresistible allure of seemingly instant and easy money. Essentially, these lottery-like payoffs, that seemed to be happening continually in 2021, aroused one of our worst human emotions: unadulterated greed. (Please see the end of the Appendix for this chapter to read a short recap of one of the highest profile examples of this phenomenon.)

These manias are in a way metaphors for the new American meme, to borrow that term, which has, in many ways, replaced the old America dream: The idea that money, success, prosperity, fame, early retirement, to be another Kevin Gill and have all of the above, whatever is your ultimate dream scenario, can be attained nearly overnight and without the typical extreme effort, like Gladwell’s oft-cited 10,000-Hour Rule.

Maybe today it’s the Fed’s ten trillion (almost) rule. If it can magically whip up trillions of fake money, why try to succeed the old-fashioned way? We’ve moved to the polar opposite of those ancient John Houseman Smith Barney ads: “They earn it!” Rather these days, it seems as though with outfits such as Robinhood it's more like “We churn it!” It wins — and Citadel wins even more — but the millions of social media market warriors who trade through them and fell for the get-rich-quick siren song, end up wiped out and even angrier than they were before they were infected with meme madness.

It’s the “something for nothing” mindset and I believe the Fed has enabled that attitude. The eight trillion it has generated literally just from its computer banks has reverberated and been amplified not only through financial markets but through much of American society. We’ve been led to believe, particularly through MMT — which, in my mind, unquestionably produced the insanity bubble — that fake money can produce real and lasting prosperity. Again, to me, nothing could be further from the truth. This has been a massive fake-out and millions have fallen for it.

To end this chapter on the modern-day madness of crowds, I thought this anecdote was an ideal capstone: Someone very lucky, or very smart, bought $8000 of a Dogecoin knockoff known as Shiba Inu (SHIB) in August of 2020. It was worth $5.7 billion 13 months later! Somehow, being a billionaire just isn’t quite as exclusive as it used to be. In my mind, the eventual post-mortem of this biggest bubble ever is almost certain to conclude along the lines of: “How could so many have been so stupid?” Except, of course, for those rare individuals savvy enough to sell into the insanity.

[i] Dogecoin was originally intended to be a satire of the cryptocurrency world. Apparently, it was designed in mere hours and its name is a play on a 2013 “meme” that went viral about a mythical spelling-challenged Shiba Inu — hence the “Doge” instead of “Dog”. Obviously, that pedigree makes it worth the $30 billion it was still valued at in late 2021. Obviously!

[ii] Around this time, one of the highest profile influencers, Dave (Davey Day Trader) Portnoy tweeted: “I’m sure Warren Buffett is a great guy but when it comes to stocks he’s washed up. I’m the captain now.”. Increasingly, it’s looking like Captain Davey is going down with his ship and his crew of similarly hubristic day traders. Meanwhile, Mr. Buffett’s Berkshire Hathaway stock recently hit an all-time high.